Table of Contents

ENDOWMENT PLAN KYA HOTA HAI?

Endowment Plan ek Tarah ka Life Insurance Plan hai jo life coverage k sath sath Saving aur Investment dono ka labh milta hai.Ye ek Tarah ka No Risk Investment Plan hai with Good Returns at Low Risk,agar Policyholder ki kisi wajah se death ho jati hai to Nominee ko ek Lumpsum amount(sum Assured+bonus)milta hai.

ENDOWMENT PLAN K BAARE ME KUCH JAANKARI

- Endowment plan me different types of plan hote hai. {Eg: Jeevan Anand(715) / Jeevan lakshya(733) / Jeevan labh(736) Etc}.Consumer aapne suvidha k anusar koi bhi Endowment plan le sakta hai jaise unki need hoti hai.

- Endowment plan me consumer apni suvidha k anusar premium (monthly/quaterly/halfyaearly,or annualy) pay kar sakta hai.

- kuch endowment plan me premium ka term duration(tenuer) fix hota hai, lekin cover period extra years k liye hota hai.(Eg:Person A koi endowment plan 21 years k liye leta hai but usko premium 15 years k liye pay karna hota hai,Policy cover time is 21 years hota hai),Kuch Endowment Plan me premium year(Duration) and Cocer period same rehta hai.

- Endowment plan ka premium term plan k premium se thoda costly hota hai, after maturity policyholder ko lumpsum amount(sumaasured + bonus) milta hai,after policyholder death ye amount nominee ko milta hai.

ENDOWMENT PLAN K BENEFITS

- Policy puri Tarah se life covered hota hai policy duration k under

- Endowment insurance plan pe aap income tax act(80C) k tahat 1.5 lakh rs tak ka benifits le sakkte hai

- isme riders addon se extra benefits milta hai

- Ye aapke k naa hone pe family ko financial security deta hai

- ye ek simple & straightforward policy hai

- Endowment Insurance plan ka premium term insurance policies k premium se kuch jyada hota hai, lekin

- sme policy maturity par policyholder ko maturity amount milta hai, or policyholder ki death pe yahi amount nominee ko milta hai

POLICYHOLDER KI DEATH HONE K BAAD SUM ASSURED(BIMA RASHI) KAI TARIKO SE NOMINEE KO MILTA HAI

Policy holder ki death hone k baad sum assured(Bima Rashi) kai tariko se Nominee ko milta hai

1. total sum assured(Bima Rashi) nominee ko milta hai or

Nominee bima rashi ko monthly quarterly halfyearly or yearly bhi le Sakata hai

2. Agar policy holder ne policy lete time ek ya ek se adhik nominee deta hai to bima rashi divide hoke milta hai.Eg: nominee A-30%, B-40%, c-30%(Ratio-A:B:C=30%:40%:30%=100%)

RIDERS ADDON(YE RIDERS AAP APNE POLICY ME ADD KAR SAKTE HAI,EXTRA CHARGES FOR ADDON RIDERS)

Life Insurance me ek optional extra service suvidha haijisko aap apne policy me add kar sakte hai jisse aapko extra benefits milte hai,niche kuch riders hai jo aap k liye benefits ho sakte hai

- Critical Illness Riders(Approx 64 diseases)- 64 types ki bimari ko cover karta hai

- Accidendal Cover-Policyholder ko isme accidental cover bhi milta hai

- Permanent Disability- Policyholder agar permanent disability ho jaye to cover milta hai

- Return of premium- Is rider ko lene se policy duration k andar policy holder ko kuch nhi hota hai to usne jitna premium pay kiya hota hai use mil jata hai.

- No Income Husband proof-ye policy women leti hai to unko apne husband ka koi income proof nhi dena hota hai.(Eg: widow,divorcee,etc)

POLICY TIME DYAN DENE WALI BAATEIN

- Jab bhi aap Term Insurance Policy ya koi bhi policy le apne family ka sath shared kare(shared with your policy)

- Policy lete time Ideal Cover(sum assured) ko apne expence k hisab se le,

Aap ko ek basic calculation provide karta hu jisse aap ideal cover amount nikal sakta hai

Life Insurance Amount= {Current year expence(65-CURRENT Age)20}/7

- Kisi bhi company ka policy buy karte time us company ka CSR(Claim Settlement Ratio) & ASR(Amount Settlement Ratio) ko jarur dhyan se dekhe

- Claim Settlement Ratio(CSR) check kariye company ka kya hai (Highest Percentage is good),CSR se jyada jaruri hai ASR check karna,kabhi kabhi kya hoya hai CSR heigest hota hai but ASR thik nhi hota ASR bhi good hona chahiye.{EG:Maan lete hai kisi company ka CSR 99% to claim to sahi hai but kya ASR kam ho, ho sakta hai wo lakh wala claim process jyada kar raha hai lekin crore wala claim process kam kar raha ho, to aapko check karna hai big amount ka claim kitna jyada hai isliye ASR check kariye

- Policy lete time company ko apni sari jankari sahi de(Give currect details,Dont hide anything to company)

ENDOWMENT PLAN(IN ENGLISH)

WHAT IS AN ENDOWMENT PLAN?

An endowment plan is a type of life insurance plan that provides both life coverage and the benefits of saving and investment. It’s a type of low-risk investment plan with good returns. If the policyholder dies for any reason, the nominee receives a lump sum amount (sum assured + bonus).

HERE IS SOME INFORMATION ABOUT ENDOWMENT PLAN.

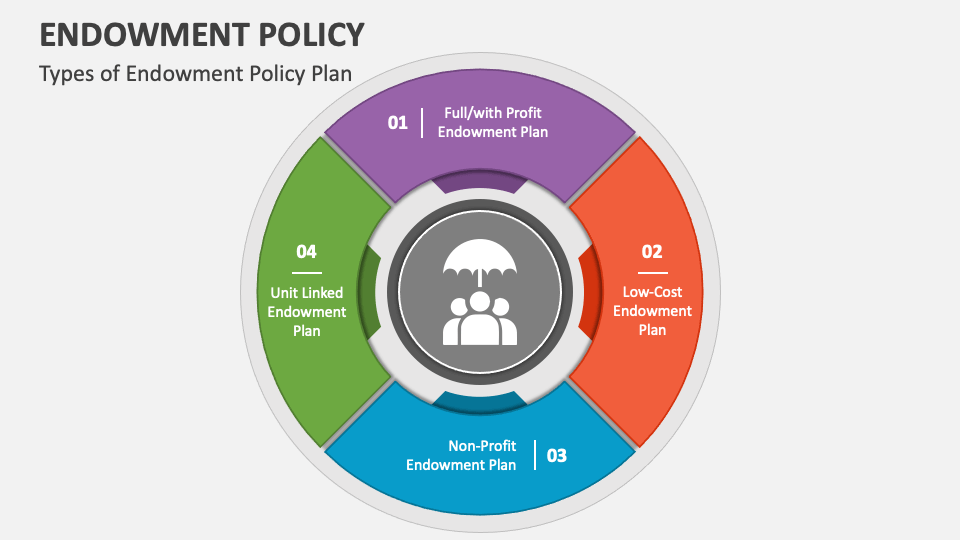

- Endowment plans come in different types. (e.g., Jeevan Anand (715), Jeevan Lakshya (733), Jeevan Labh (736), etc.). Consumers can choose any endowment plan according to their convenience and needs.

- In an endowment plan, consumers can pay the premium according to their convenience (monthly, quarterly, half-yearly, or annually).

- In some endowment plans, the premium payment term (tenure) is fixed, but the cover period extends for extra years. (For example, Person A takes an endowment plan for 21 years, but they only have to pay premiums for 15 years; the policy cover time is 21 years). In some endowment plans, the premium payment period and the cover period are the same.

- The premium for an endowment plan is slightly more expensive than that of a term plan. After maturity, the policyholder receives a lump sum amount (sum assured + bonus). After the policyholder’s death, this amount is paid to the nominee.

BENEFITS OF ENDOWMENT PLAN

- The policy provides complete life coverage during the policy duration.

- With an endowment insurance plan, you can avail tax benefits of up to ₹1.5 lakh under the Income Tax Act (Section 80C).

- It offers extra benefits through riders/add-ons.

- It provides financial security to your family in case of your untimely demise.

- This is a simple and straightforward policy.

- The premium for an endowment insurance plan is slightly higher than that of term insurance policies, but with this policy, the policyholder receives the maturity amount upon policy maturity, and in case of the policyholder’s death, the same amount is paid to the nominee.

AFTER THE POLICYHOLDER’s DEATH, THE SUM ASSURED (INSURANCE AMOUNT) IS PAID TO THE NOMINEE IN SEVERAL WAYS.

After the policyholder’s death, the sum assured is paid to the nominee in several ways:

- The total sum assured is paid to the nominee, and

The nominee can receive the sum assured monthly, quarterly, half-yearly, or annually. - If the policyholder designates one or more nominees at the time of purchasing the policy, the sum assured is divided among them. For example: Nominee A – 30%, B – 40%, C – 30% (Ratio – A:B:C = 30%:40%:30% = 100%)

RIDERS (THESE RIDERS CAN BE ADDED TO YOUR POLICY, EXTRA CHANGES APPLY FOR ADD-ON RIDERS)

Life insurance offers an optional extra service that you can add to your policy to receive additional benefits. Below are some riders that might be beneficial for you:

- Critical Illness Riders (Approximately 64 diseases) – Covers 64 types of illnesses.

- Accidental Cover – The policyholder also receives accidental coverage.

- Permanent Disability – Provides coverage if the policyholder becomes permanently disabled.

- Return of Premium – With this rider, if nothing happens to the policyholder during the policy term, they receive a refund of the premiums paid.

- No Income Proof for Husband – If a woman takes out this policy, she does not need to provide any income proof for her husband. (e.g., widow, divorcee, etc.)

THINKS TO KEEP IN MIND WHEN BUYING A POLICY

- Whenever you take out a Term Insurance Policy or any other policy, share the details with your family.

- When taking out a policy, choose the ideal cover (sum assured) based on your expenses.

- Here’s a basic calculation to help you determine the ideal cover amount:

Life Insurance Amount = {Current year expenses * (65 – Current Age) * 20} / 7-

- When buying a policy from any company, be sure to carefully check the company’s CSR (Claim Settlement Ratio) and ASR (Amount Settlement Ratio).

- Check the company’s Claim Settlement Ratio (CSR) (the highest percentage is good). Checking the ASR is even more important than checking the CSR. Sometimes, the CSR is high, but the ASR is not good. The ASR should also be good. (For example: Let’s say a company has a CSR of 99%, so the claims are being processed correctly, but the ASR might be low. It’s possible they are processing more claims for smaller amounts (in lakhs) but fewer claims for larger amounts (in crores). So, you need to check how many claims for large amounts are being processed. That’s why you should check the ASR.)

- When taking out a policy, provide all your information correctly to the company (Give correct details, don’t hide anything from the company).